By WJ Rossi, Brian Watson and Ben Doty

“Courage is not the absence of fear. It is going forward in the face of fear.” – Abraham Lincoln

These are challenging times for all of us. We have high numbers of unemployed citizens, businesses have temporarily or permanently closed, and, of course, the specter of testing positive for COVID-19 and what will happen to you are ever present. And, this is not an exhaustive list of all the very real, personal challenges many have. One sliver of crisis, hardly as daunting as that related to health and bankruptcy, but still informative, is the one we deal with in our business, the impact on financial goals from events such as these. In fact, the first half of what happened this year is instructive of “going forward in the face of fear” for events of longer duration. While the economy is not going through a V-shaped recovery, financial markets, more or less, have up to this point. And what we saw was that most people we work with did not pull the plug on their financial plans and investments as markets plunged in February and March.

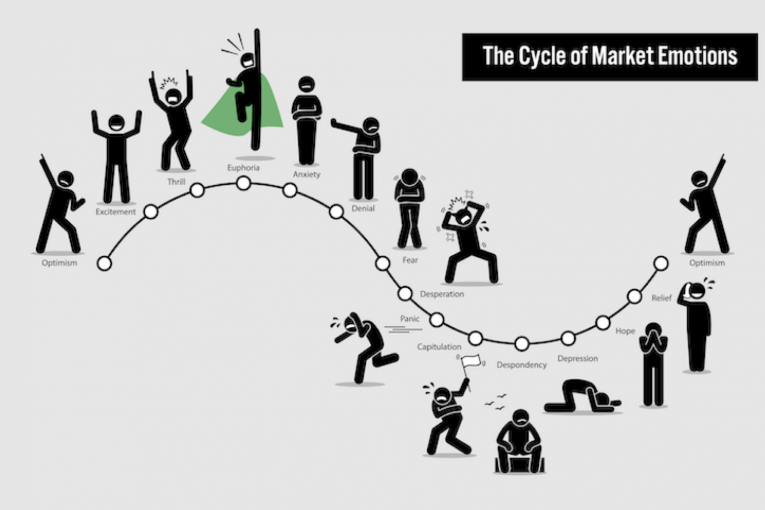

Certain psychological, behavioral biases often make us give into fear with a flight response, when a fight response may be more appropriate. One such bias in finance is called the recency bias, when investors overemphasize recent events over past events. Recent events we can think of are price drops. When stock prices fall, most investors expect more declines. This corresponds with anxiety and, eventually, fear and desperation. Investors may decide to go into a flight mode and make their investments conservative.

Recency bias often works with confirmation bias, which involves accepting information that confirms beliefs and discounting information that contradicts. An example may be pointing to recent price drops as confirmation that your fears are well-founded. Or it could be focusing on the most negative news, comparing the impact on the economy to what happened during the Great Depression. It might cause you to discount information suggesting the market may be priced for opportunity not decline. Questioning what feels easy to believe goes to the heart of Warren Buffet’s quote – “Be fearful when others are greed and be greedy when others are fearful.”

For better or worse, these biases cluster with others, such as loss aversion bias, hindsight bias, anchoring, overconfidence, and the narrative fallacy. Loss aversion, or the regret bias, is our preference to avoid a loss because the associated pain is more intense than the reward felt from a gain. A 5% recent daily decline is far more emotionally powerful than a 5% rise. Loss aversion made the series of declines in early March far more powerful than the equal comebacks the next day. An obsession with bad news can accelerate panic. That is why we caution people about focusing much, if at all, on quarterly returns, much less daily or monthly changes in the market. It’s the same return but viewed less often, one sees it for more of the positive outcome that it is. The probability of seeing a negative return, decreases with the frequency you watch your portfolio or the market. In fact, the probability of losing money decreases from 46% daily to 25% annually when you look at data over the last 10 years. It is one way to push back against loss aversion by not looking so often.

Probability of Losing Money in the Market: 2000 to 2019

People most often think they are right when making decisions. For every seller of Tesla, for example, there is a buyer. And they both think they are getting a good deal. Of course only one of them is right. Your odds of being on the right side of a decision may improve by understanding your behavioral biases, especially in times of crisis.

WJ Rossi and Brian Watson are Partners at Koss Olinger. Ben Doty is a Senior Investment Director at Koss Olinger.

Disclosures: The opinions should not be construed as specific investment advice. All information is believed to be from reliable sources, however, no representation is made to its completeness or accuracy. All economic and performance information is historical and not indicative of future results. The S&P 500 and other benchmark indices are not directly investable indices.